Introduction

The following text elaborates on the 2018 budget implementation of the Fabrique d’église (FE). An important caveat needs to be mentioned. From 2019 onwards, the FE started to follow the guidance of the Region Bruxelles-Capital, according to which the accounting needs to strictly follow the calendar year. This means that in a given year, only those transactions which already impacted the bank account can be recorded. Previously a different practice had been applied whereby the transactions had been allocated to the year where they belonged. So for example, if an invoice for electricity came in December but was actually paid only in January, it would still be imputed to the December expenditures. This change of practice impacts several items hence comparisons between 2017, 2018 and 2019 need to be done with care.

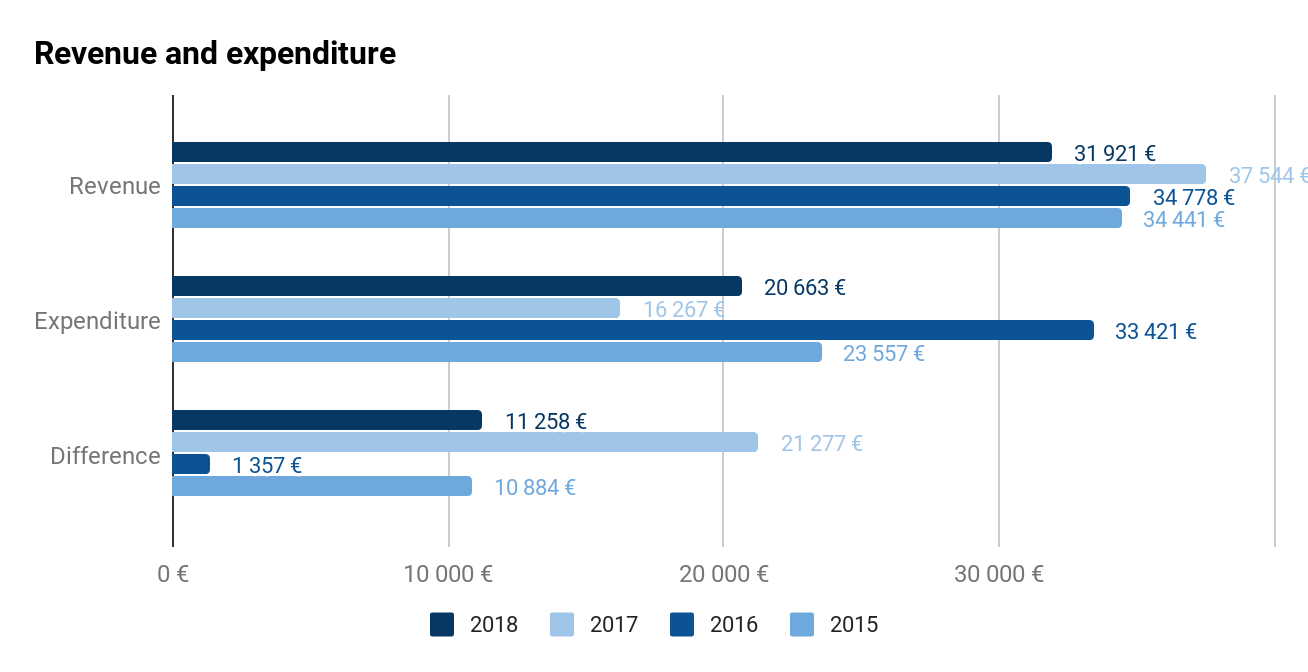

The balance of revenues and expenditures

In 2018, the FE reached a surplus of 11 258 €, which was lower than in 2017. On the revenue side this was mainly due to a shortfall of rental revenue and methodological changes (see below). The expenditures were on the other side higher especially due to a refurbishment of the church apartment (see below) and higher heating costs.

Revenue

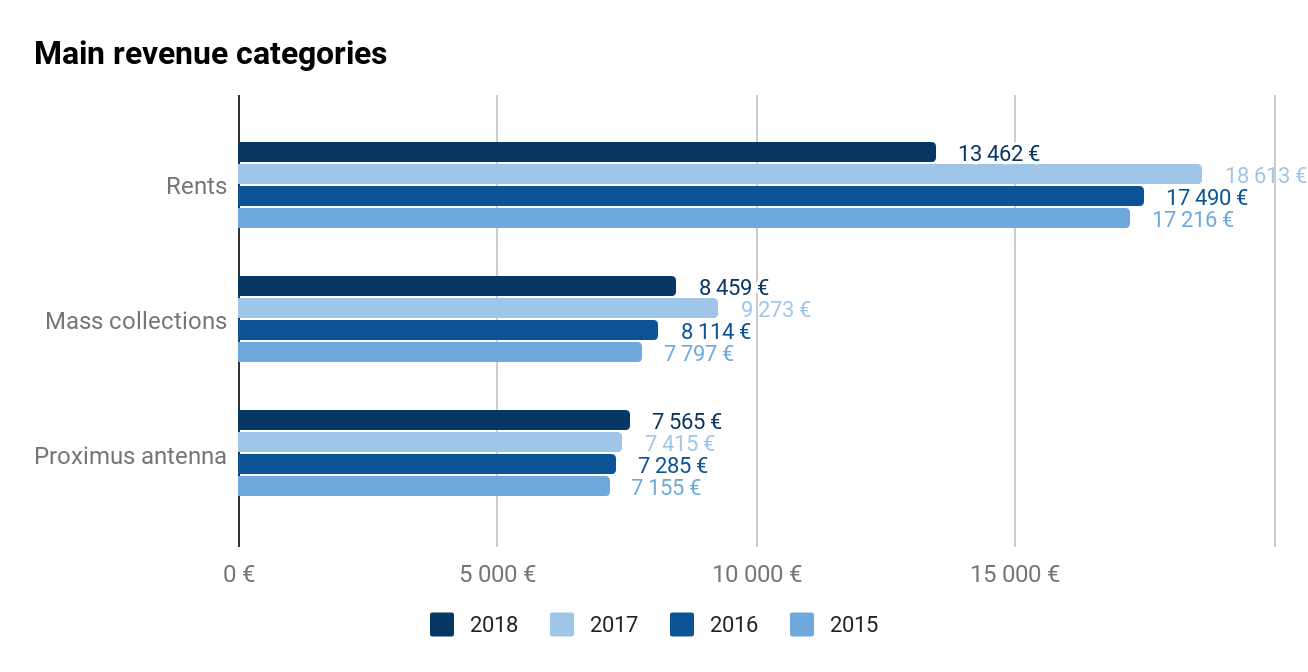

- Rents: Rental revenues come from two sources – the rental of the apartment next to the church and the contribution of abbé Charles Declercq living in the presbytery. In 2018 the reported rental revenue was well below the 2017 level. The reason is twofold. The first one is the departure of the previous tenant in the apartment next to the church in June. The apartment required several urgent improvements (e.g. kitchen, bathroom), which were carried out in the period July-November. The new tenant, therefore, moved in only in December 2018. The second source of the shortfall is more artificial and is connected to the delayed payment of the part of the rent by abbé Declercq only in January 2019. Given the methodological changes, this revenue was not recorded in 2018 accounts.

- Mass collections: The observed drop in the collections is from the largest part again due to the methodological change (i.e. 2018 December collections were transferred to the bank account only in January 2019). Abstracting from this change there would be a small growth. The size of collected contributions during masses is sensitive to Sundays when the collection takes place because during holiday periods the number of faithful on Sunday masses drops dramatically as all communities are foreigners. Nevertheless, it seems that the level of mass collections has stabilized at somewhat above 9 000 €.

- Proximus antenna: A third important source of revenue is rent paid by Proximus for placing their antenna in the church tower. The annual rental is indexed every year and in 2018 it amounted to 7 565 €.

- Donations: This category includes regular and one-off donations. In 2018 increase considerably by 1 200 € which was due to a one-off donation resulting from the sale of unused furniture of one of the community members.

- Others: This category includes smaller revenue flows such as donations on specific purpose (e.g. flowers), celebration fees (e.g. funerals) and interest revenue.

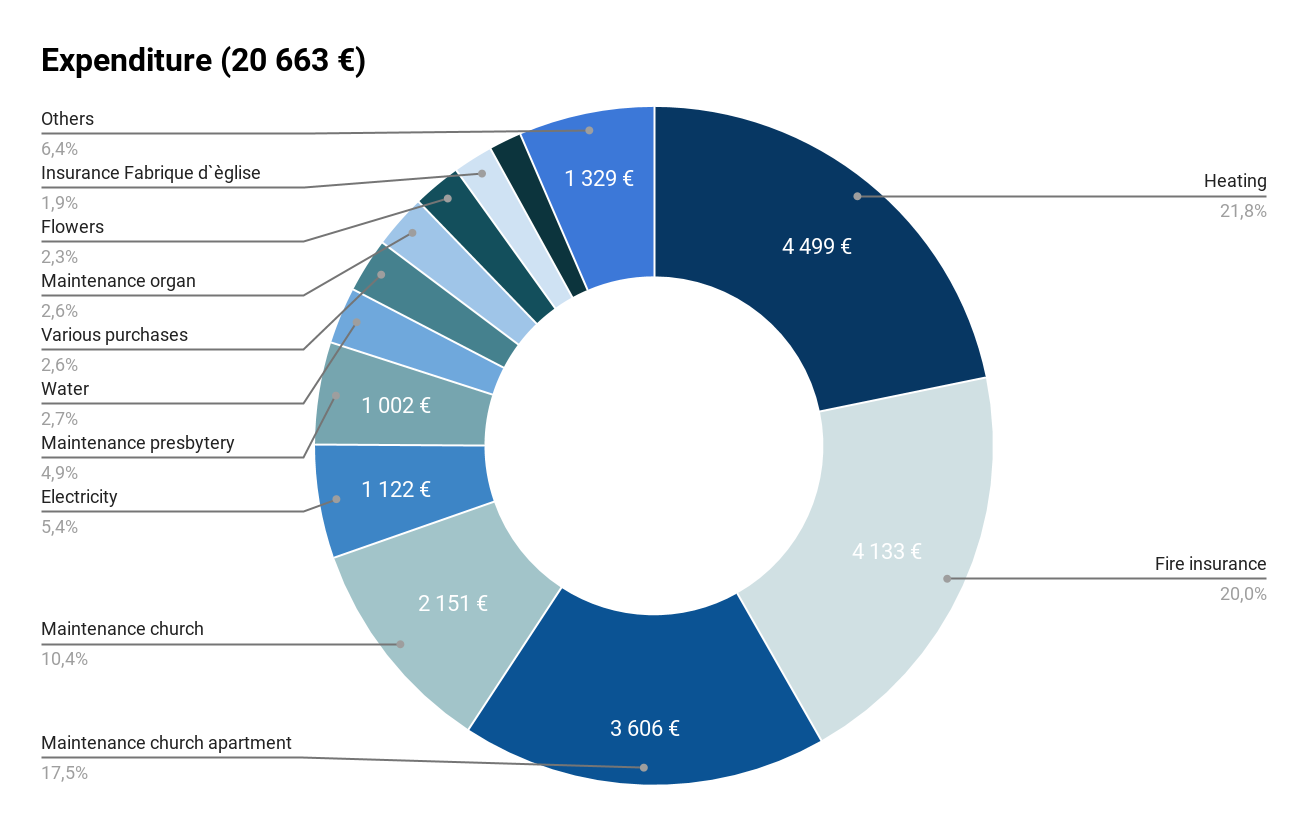

Expenditures

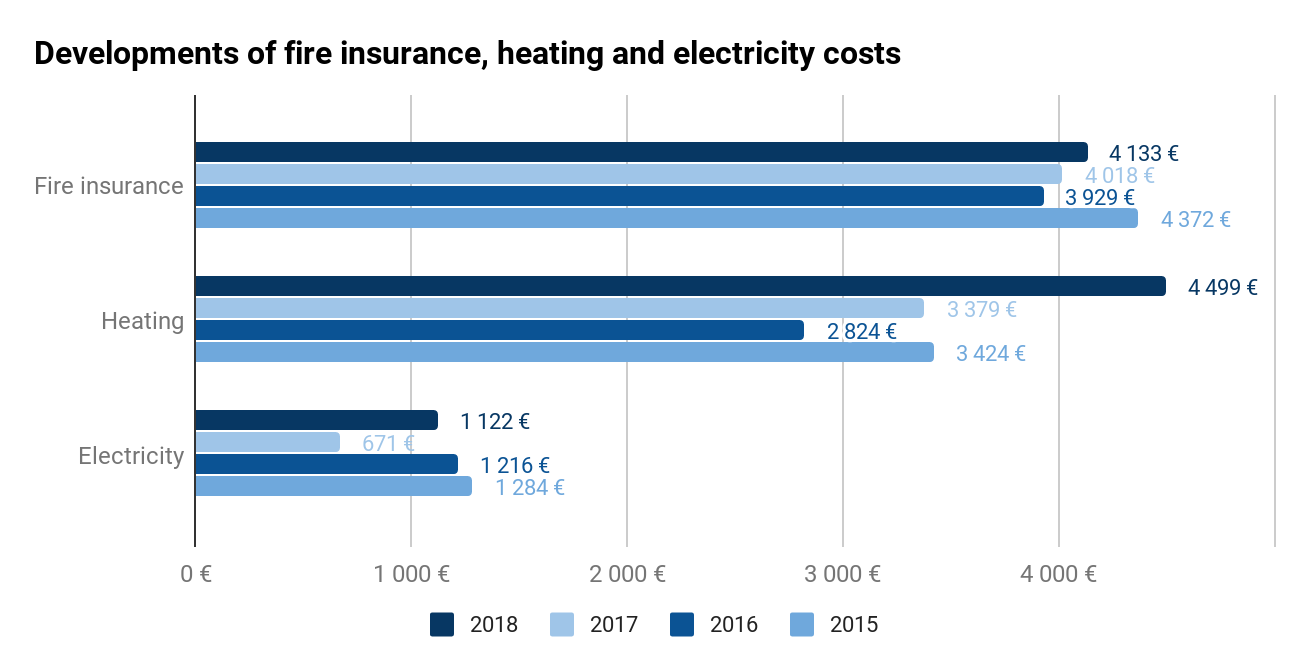

- Insurance: Fire insurance is one of the largest recurring items. It covers both the church and the presbytery. While the FE managed to reduce the prime by more than 10% in 2016, the insurance has increased again since then and in 2018 constituted 20% of all spending.

- Heating: Heating costs constitute another important recurring outlay. In recent years they have increased. The most obvious reason is the arrival of the Polish community in autumn 2017 which lead to an increase in gas consumption. In the medium term, the FE will explore the possibility of changing the furnace to increase the efficiency of heating.

- Electricity: The electricity expenditures have declined over the years especially due to the use of more efficient light bulbs. The project to redo the electricity in the whole church should increase the efficiency further in coming years. Another project that may contribute to lower electricity invoices is placing of solar panels on the church roof in the medium term.

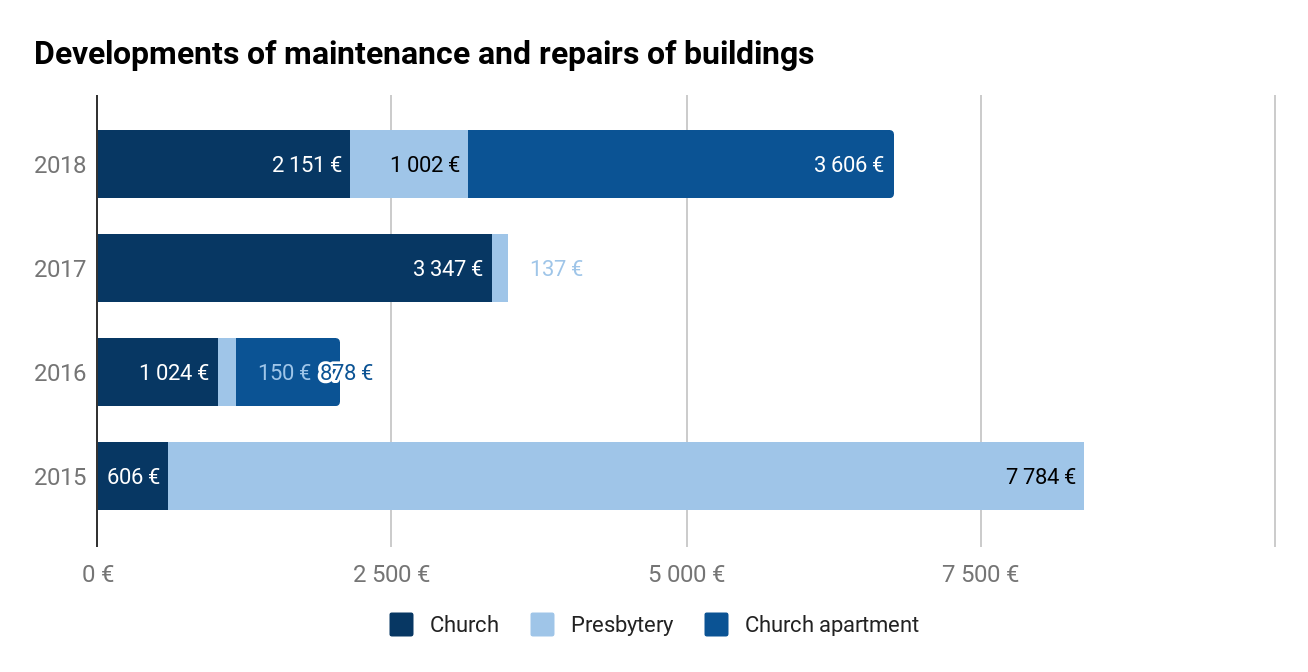

- Maintenance: Spending on maintenance is not a stable expenditure item as it reflects actual needs in a given year. Repairs often address underinvestment in the past years which now require immediate action.

- Church apartment: In 2018, the degraded kitchen and partly a bathroom of the apartment next to the church were refurbished (new kitchen furniture was also purchased) to make them habitable for new tenants who moved in December 2018. The overall costs reached some 3 600 €.

- Church: An important item in the church maintenance is the annual revision of the furnace which in 2018 cost almost 700 €. Another outlay that has become recurring in past years is repair of the roof, which needs a major overhaul. In 2018, roof reparations cost 1 452 €.

- Presbytery: The repairs in the presbytery have been kept to a minimum in the past years. The last larger investment took place in 2015 when the issues with the canalization in the underground were fixed.

- Various purchases: While this category is not often used, in 2018 it includes a purchase of a lapel microphone demanded by the Polish community which cost 454 €.

- Maintenance organ and bells: While the bells have been checked annually for several years now, regular servicing of the organ started only in 2016 after several issues occurred. The servicing of the organ costs some 530 €. Servicing of bells is somewhat cheaper at 250€ per annum and is hence included in the category ‘Others’.

- Insurance FE: The FE has a third party liability insurance which amounts to a little less than 400 € annually.

- Others: This category contains smaller spending items such as hosts, vine, candles, cleaning of the church. etc.

Annexes